Insider Spotlight

Signs of renewed strategic direction are emerging across the sector, driven by reforms that strengthen investor confidence and an economic landscape that is steadily diversifying beyond Metro Manila.

A fresh report from Santos Knight Frank highlights how long-horizon policies, the rise of new growth corridors, and accelerating demand for next-generation assets—from data centers to luxury residences—are collectively reshaping the country’s property landscape for more resilient and sustainable expansion.

Rick Santos, chair & CEO of Santos Knight Frank, underscores the significance of 2025’s structural recalibration.

“Looking at 2025, it’s clear that this has been a year marked by purposeful pivots and structural shifts across the Philippine real estate landscape,” he said in a press statement.

“The signing of the 99-year land lease into law, along with progressive amendments to the REIT framework, signals a strong policy environment—one that broadens the universe of acceptable assets and unlocks new channels for long-term investment.”

99-year land lease: A long-game catalyst

One of the year’s most consequential developments is the passage of the 99-year land lease law—a reform expected to significantly elevate the Philippines’ investment credentials.

By providing long-term tenure security, the measure widens the financing options for major development projects and increases the country’s attractiveness to institutional investors.

More critically, the extended lease regime aligns the Philippines with ASEAN neighbors already offering similar terms. This positions the country more competitively for foreign direct investment, while deepening opportunities for joint ventures, REIT expansion, and large-scale masterplanned communities.

Demand for land in prime growth corridors is projected to accelerate as a result, setting the stage for higher land values and more ambitious developments in the years ahead.

Office market: Rebounding on IT-BPM demand

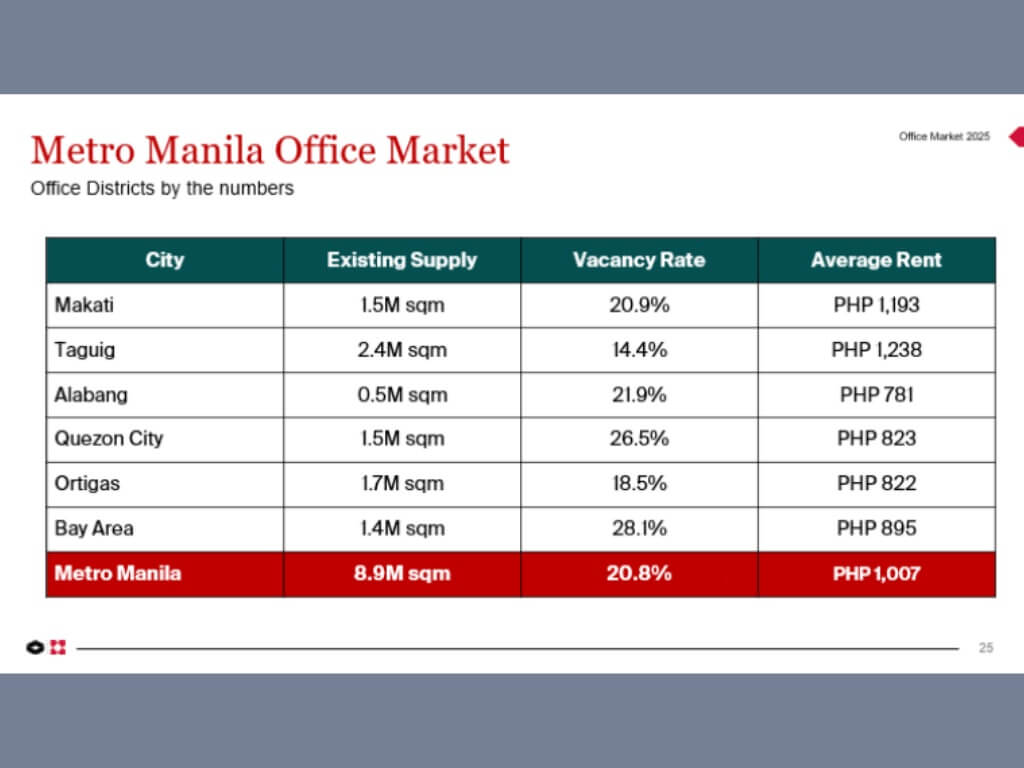

Despite global headwinds, the IT-BPM industry continues to power the office sector. Year-to-date net absorption reached 461,245 sq.m., lifting Metro Manila’s office stock to 8.9 million sq.m., with 328,000 sq.m. added as of November.

The development pipeline remains robust, with 1.5 million sq.m. scheduled for completion through 2029—primarily in Quezon City, Taguig, and Ortigas. Vacancy sits at 21 percent, while Taguig commands the highest asking rent at P1,242/sq.m./month, 23 percent above the Metro Manila average.

Santos notes the country’s shifting geography of growth. “We’re seeing growth decentralize, with major developments rising in Cebu, Pampanga, Davao and New Clark City—signaling a more diverse economic trajectory,” he says.

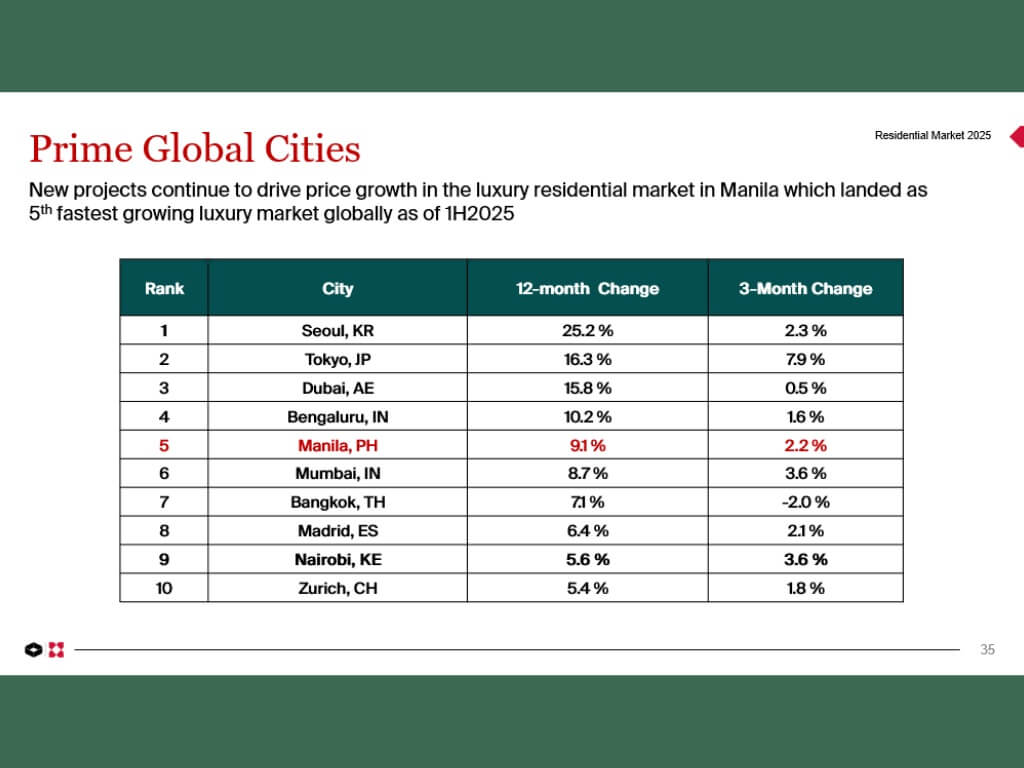

Meanwhile, Manila continues to punch above its weight in the global luxury space, ranking 5th in Knight Frank’s Prime Global Cities Index, buoyed by a 9.1-percent year-on-year increase in prices.

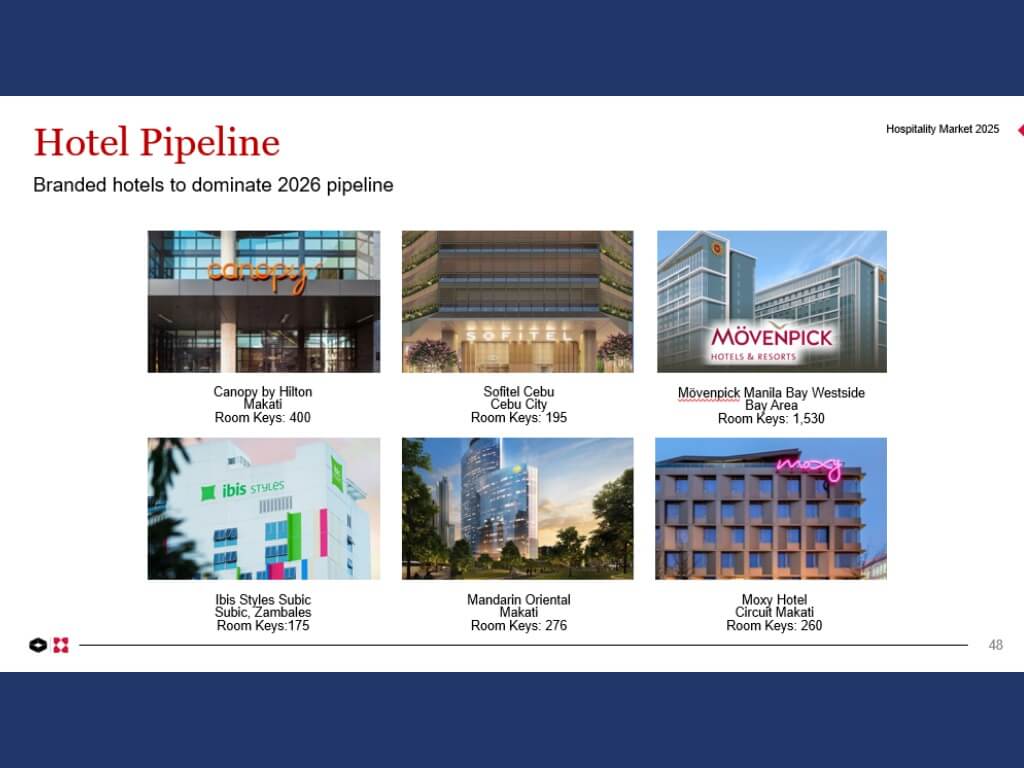

Hospitality: A banner year for big-brand openings

The hospitality sector is experiencing one of its strongest cycles in years. With tourist arrivals hitting four million and the government pushing enhancements such as the VAT refund program and expanded visa-free entry, global operators have doubled down on Philippine expansion.

Accor, Marriott, and Banyan Tree opened multiple properties in 2025, with more high-end offerings—Canopy by Hilton, Sofitel’s redevelopment, Mövenpick Manila Bay, and the Mandarin Oriental—set to deepen the country’s luxury footprint.

Concurrent investments in MICE infrastructure through SMX Seaside Cebu, Mactan Expo Center, and the Bohol International Convention Center are raising the country’s competitiveness in the regional meetings and events circuit.

Industrial market: Data centers lead the next wave

The industrial sector is undergoing a major transformation, moving beyond traditional warehousing into specialized formats such as cold storage, smart manufacturing hubs, and—most notably—data centers.

The Department of Information and Communications Technology projects the Philippines’ data center capacity to reach 1.5 GW by 2028, driven by digital transformation and cloud adoption. Calabarzon and Central Luzon continue to dominate new estate launches, benefiting from proximity to ports and the NCR.

Retail: Provinces rise, global brands expand

Following trends in residential development, provincial malls are entering a new expansion phase, with developers rolling out large-format retail destinations in emerging growth cities. Northern Luzon and Southern Mindanao lead the charge on consumer-driven optimism.

Global brand activity also surged, supported by improvements in ease of doing business. Lifestyle labels such as Maje, Sandro, Alice + Olivia, and sports/hobby names like Alo, Oysho, and Wilson expanded aggressively.

High-end F&B concepts—including Smith & Wollensky, Niku Niko Oh!! Kome, and Dave & Buster’s—also made their Philippine debut.

Santos frames 2025 as a pivotal year of renewal. “Through these shifts, the Philippines remains a market defined by resilience, reinvention, and untapped potential. And even amid calibration, 2025 presents clear silver linings—opening new pathways for renewed confidence and long-term, sustainable growth.” —Ed: Corrie S. Narisma