Jollibee Foods Corp. (JFC) is reining in growth plans after soaring commodity and supply chain costs dragged first quarter profits sharply lower despite continued strong consumer demand across its Philippine and international businesses.

The fast food giant said it is reviewing the pace of store openings, capital spending and profitability expectations for 2026 as the Middle East conflict fuels fresh volatility in global commodity and supply chain costs, complicating its rapid international expansion plans.

“Jollibee Group is reviewing certain 2026 assumptions, including the pacing of store openings, planned capital expenditures, and profitability expectations, while actively implementing mitigation actions across sourcing, productivity, selective pricing, and disciplined cost management,” the company said in stock exchange filing.

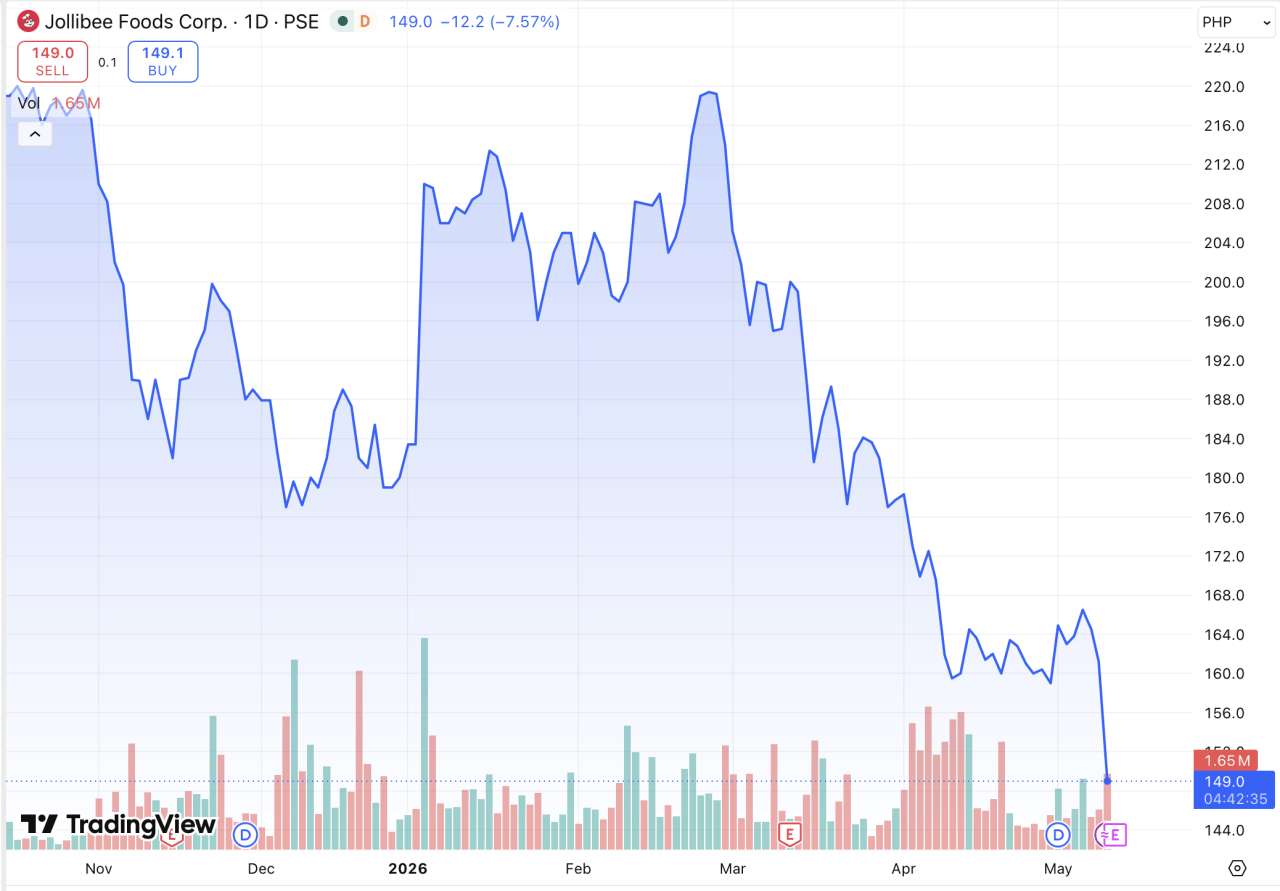

JFC shares tumbled as much as 8.8 percent in early morning trade. At its latest price of P149.3, the stock is down about 17 percent since the start of 2026.

Price hikes ahead

Jollibee plans price hikes and tighter cost controls beginning in the second quarter.

“We are taking disciplined steps to manage near-term volatility through measured price increase beginning in Q2, alongside thoughtful and targeted cost management initiatives, while continuing to advance sustainable growth and long-term shareholder value,” president and CEO Ernesto Tanmantiong said in the filing.

Strong sales, profits tumble

First quarter net income plunged 38.8 percent to P1.5 billion even as systemwide sales climbed 10.3 percent to P113.9 billion and revenues rose 9 percent to P76.5 billion.

Operating income fell 18.2 percent to P3.9 billion, while earnings before interest, taxes, depreciation and amortization (EBITDA) slipped 4.9 percent to P9.3 billion as soaring food, freight and supply chain costs outpaced sales growth.

Its EBITDA margin, a measure of profitability, narrowed 170 basis points to 12.2 percent after direct costs surged 11.7 percent amid inflation in commodities and broader geopolitical disruptions.

Expansion meets resistance

The sharp earnings decline marked a growing challenge for Jollibee, which has spent years aggressively expanding its global footprint through rapid store openings and overseas acquisitions.

The company opened 181 gross new stores during the quarter, including 149 international locations, pushing its global network to 10,421 stores worldwide.

International sales jumped 13.5 percent, faster than the Philippines’ 8 percent growth, driven by Compose Coffee, Highlands Coffee, Tim Ho Wan and Jollibee’s Middle East operations.

Jollibee’s flagship brand remained the group’s main growth engine, posting 10.7 percent global systemwide sales growth and 4.2 percent same-store sales growth.

Balance sheet remains solid despite challenges

Jollibee’s balance sheet showed the growing financial weight of its rapid global expansion, even as the company maintained a relatively stable asset base and manageable short-term liabilities.

Cash and cash equivalents fell 20.1 percent to P27.9 billion while long-term debt more than doubled to P33.4 billion as the fast food giant continued funding overseas expansion, acquisitions and store network growth.

Profitability takes center stage

The company also continued restructuring weaker overseas businesses, including strategic Smashburger conversions and China’s shift toward a higher-return franchising model aimed at improving returns and reducing capital intensity.

“First-quarter profitability was impacted by temporary cost pressures. Underlying demand across the business remained healthy. We view these headwinds as manageable, supported by disciplined cost controls, ongoing productivity initiatives, and targeted margin recovery actions across our brands and markets,” chief financial and risk officer and Jollibee Group International Business CEO Richard Shin said.

“We are managing today’s cost volatility prudently, and we remain confident in our long-term growth outlook. As costs normalize over time, we remain focused on prudent capital allocation and sustaining profitable, long-term growth,” he added.

—Edited by Miguel R. Camus