Inside Mynt’s IPO: GCash growth, profits and key investor risks

June 27, 2026

9:24PM PHT

Share

Here are the most important takeaways from Mynt’s 592-page preliminary prospectus that matter most ahead of its planned IPO.

The big picture

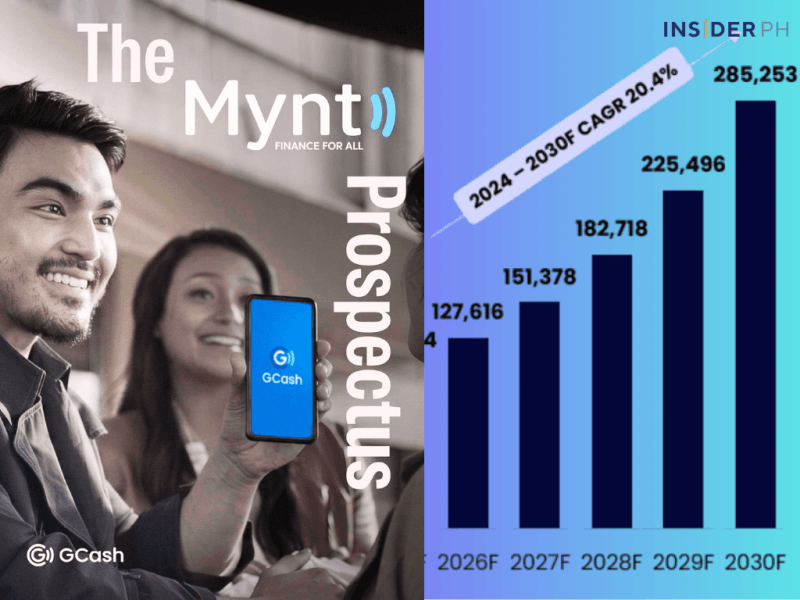

The largest Philippine IPO on record. Mynt plans to raise up to P80.3 billion through the sale of up to 8.03 billion shares, with an additional 1.2 billion-share overallotment option. At the maximum offer price of P10 per share, the deal could reach roughly P92.3 billion including the greenshoe.

Implied valuation exceeds P660 billion. At the maximum IPO price, Mynt would be valued at roughly P669 billion (about $11 billion), making it one of Southeast Asia’s most valuable fintech companies.

Most of the IPO is existing shareholders selling. Of the P80.3-billion base offering:

about P14.9 billion in net proceeds will go to Mynt from newly issued shares;

about P74.3 billion (assuming full overallotment) will go to selling shareholders, not the company.

Data from the Mynt prospectus

What the company says makes it valuable

Mynt positions itself not simply as an e-wallet but as the Philippines’ leading finance super app, with GCash serving as the gateway to payments, lending, savings, investments and insurance.

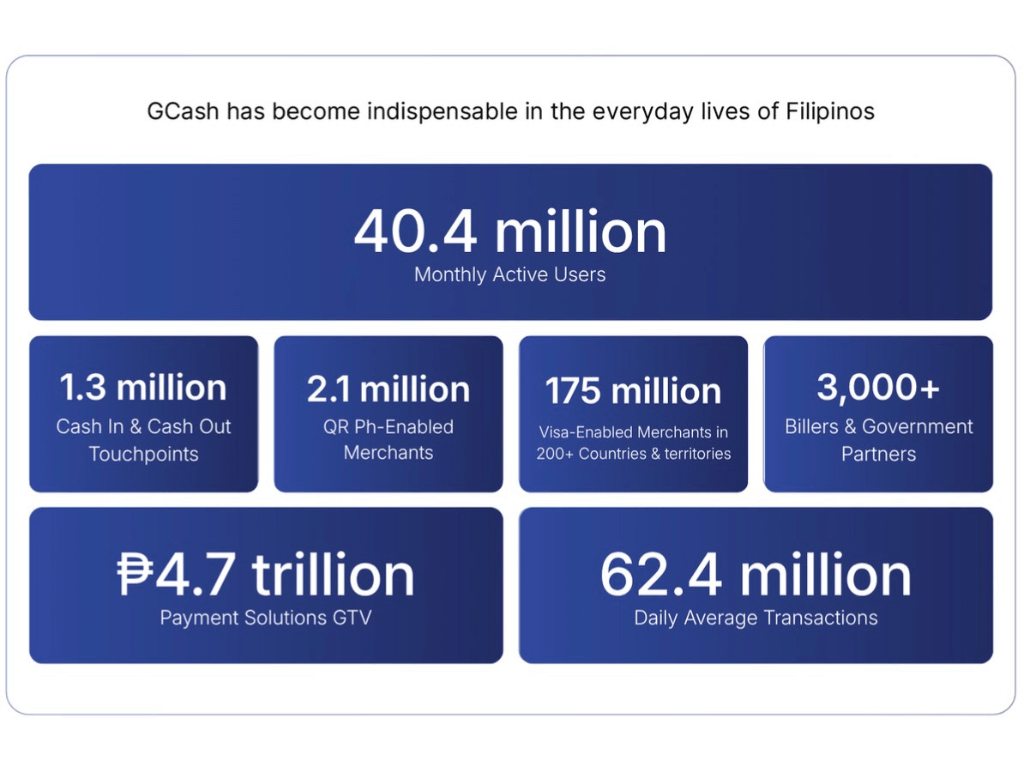

Key operating metrics as of March 31, 2026:

40.4 million monthly active users, equivalent to almost 55 percent of Philippine adults

4 times the active users of its nearest competitor

62.4 million daily average transactions

2.1 million QR merchants

1.3 million cash-in/cash-out locations

Presence across 175 million Visa merchants in over 200 countries and territories and more than 3,000 billers and government partners.

Financial performance

The prospectus highlights rapid profit growth.

Adjusted revenues

2023: P33.6 billion

2024: P54.1 billion

2025: P79.7 billion

Net income

2023: P6.38 billion

2024: P11.13 billion

2025: P17.25 billion

For the first quarter of 2026:

Revenue rose to P20.74 billion

Net income increased to P5.6 billion, from P4.52 billion a year earlier.

Data from the Mynt prospectus

Scale of the payments business

Payment volume remains the company’s biggest strength.

P17.03 trillion in payment solutions gross transaction value (GTV) in 2025

P4.75 trillion GTV during the first quarter of 2026 alone, up 23.2 percent year on year.

Growth beyond payments

GCash has expanded into financial services:

7.5 million active borrowers

16.9 million savings account users

9 million investment fund users

1.9 million users investing in Philippine stocks.

Where IPO proceeds will go

The company says proceeds from the primary shares will fund:

expansion of its CreditTech business;

product development;

strategic cash reserves; and

general corporate purposes.

Data from the Mynt prospectus

Key investor watchpoints

Several issues stand out for investors:

Large secondary sale. Roughly 80 percent of the base offering consists of existing shares, meaning most IPO proceeds benefit current shareholders rather than fund new expansion.

Heavy dependence on lending growth. A significant portion of future growth is expected to come from CreditTech, making loan quality an important metric.

Regulatory exposure. The company acknowledges risks from BSP regulation. The glossary specifically references the BSP directive requiring removal of gambling links from payment apps in 2025, illustrating how regulatory actions can affect revenue streams.

Competition. Although GCash is the dominant player today, maintaining leadership against digital banks, e-wallets and other fintech platforms remains a key challenge.

IPO structure

Maximum offer price: P10 per share

Ticker: GCASH

Institutional allocation: 70 percent

Retail and trading participant allocation: 30 percent (20 percent through brokers and 10 percent for Local Small Investors)

Proposed pricing date: around September 28, 2026

Expected retail settlement: around October 9, 2026, subject to regulatory approvals.

Bottom line

The prospectus presents Mynt as a company that has evolved beyond payments into the Philippines’ dominant digital financial ecosystem. Investors are being asked to value it on continued growth in lending, wealth management and merchant services, rather than payments alone. At the same time, the IPO’s structure—with the majority of shares coming from existing investors—and its premium valuation are likely to be central questions during the book-building process.