Backed by conglomerates such as Manuel V. Pangilinan-led Metro Pacific Investments, Consunji-led DMCI Holdings, and Japan’s Marubeni, Maynilad priced its IPO at P15 per share, below the initial reference price of P20 apiece.

This values the deal at P34.3 billion, making it the largest Philippine Stock Exchange listing since food giant Monde Nissin’s nearly P49-billion debut in 2021.

Maynilad is led by its longtime president and CEO Ramoncito Fernandez.

What’s next?

The final pricing followed talks with major institutional investors, including the International Finance Corp. (IFC) and the Asian Development Bank (ADB), securing sufficient commitments for Maynilad to proceed with the offer at P15 per share, valuing the firm at around P113 billion.

The large investor tranche was about 1.8 times oversubscribed, according to earlier reports by InsiderPH’s INSIDER INFO.

The official sale period will run from Oct. 23 to 29, with trading debuting on the Philippine Stock Exchange under the ticker “MYNLD” on Nov. 7.

AP Securities: Maynilad IPO is a buy

Alfred Benjamin R. Garcia, research head at AP Securities, issued a “subscribe” rating on Maynilad, citing strong earnings and “generous” dividends.

“We believe that the offer is prudently priced and offers sufficient, albeit modest, upside to garner investor interest,” Garcia said in a report dated Oct. 21, 2025.

He said their discounted cash flow model gives a base value of P16.14 per share, reflecting Maynilad’s projected future earnings.

The multiples-based approach points to a potential upside of P20.40 per share, assuming market sentiment improves and valuations normalize, he explained.

Meanwhile, Garcia sees limited downside at P12.32 per share based on their “worst-case scenario” model.

Not just any defensive play

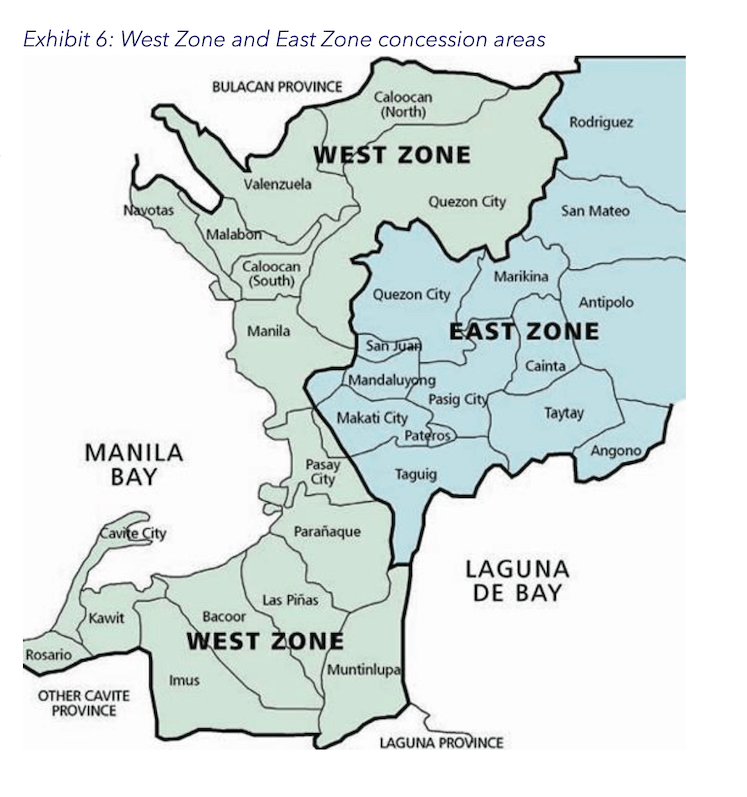

Garcia noted that population growth in Maynilad’s concession area, covering the West Zone of Metro Manila, home to about 10.5 million people, supports the company’s long-term demand outlook.

“As such, MYNLD is poised to join the small club of truly defensive plays in the market,” he said.

“On top of this, MYNLD also has a dividend policy in place that could deliver a dividend yield of 5.8 percent in 2026, increasing its appeal to investors with lower risk appetites,” he added.

He added that scheduled water tariff hikes through 2027 are expected to boost Maynilad’s revenue stability and support long-term valuation growth.

Prime Water deal?

Garcia also flagged risks, noting that Maynilad’s heavy reliance on its West Zone operations adds concentration risk, as nearly all its revenue comes from that area.

He also views the possible acquisition of the Villar Group’s Prime Water as a potential risk rather than an opportunity for diversification, given the steep premium reportedly demanded for the sale.

Big picture

Maynilad is the second and largest PSE listing in 2025, following the debut of Erik Lim-led Top Line Business Development.

Over P25 billion from the IPO proceeds will be used to fund expansion and capital expenditures, as part of its multi-year infrastructure plan.

Maynilad has outlined P105 billion in capital spending through 2027, down from the P163 billion budget it initially announced for 2023–2027.

The company is investing in new water sources and treatment facilities, operations support, and reducing water losses through non-revenue water management and service expansion.

Miguel R. Camus has been a reporter covering various domestic business topics since 2009.