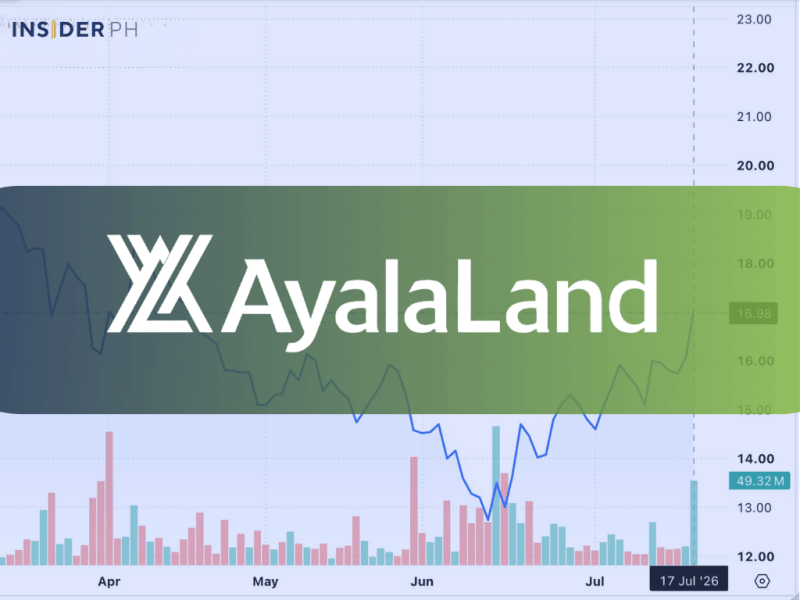

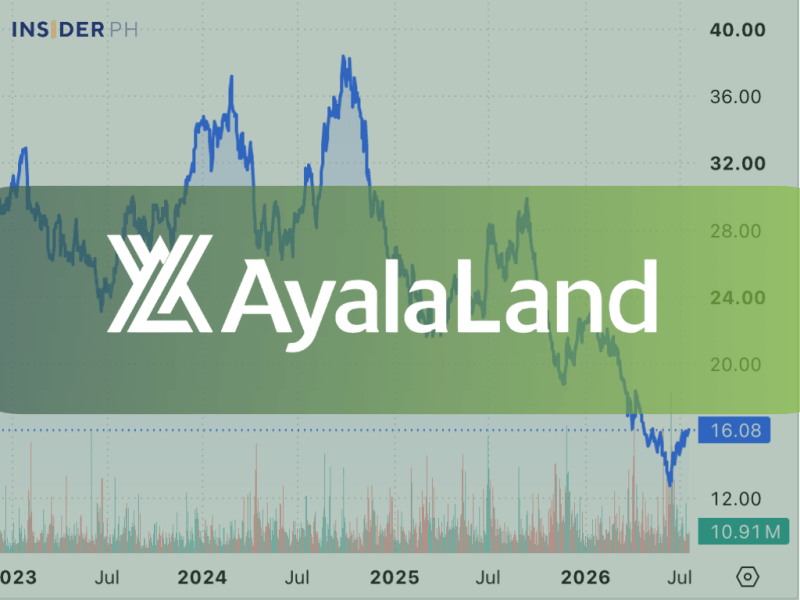

• Ayala Land cut to “hold” from “buy” as First Metro slashed its target price by nearly 45 percent to P15.50 from P28.

• Debt remains higher than many peers, a factor First Metro said could limit Ayala Land’s flexibility to pursue more aggressive expansion.

• Valued at just 0.6 times book value, implying the stock deserves to trade about 40 percent below the net value of its assets.

One of the country’s biggest property names received a rare downgrade from top broker First Metro Securities (FMS), which said mounting pressures on its core housing business and a heavy debt maturity schedule have fundamentally altered its outlook.

FMS downgraded Ayala Land (ALI) to “hold” from “buy” and slashed its target price by almost half to P15.50 from P28 apiece, saying the challenges facing the company now justify a sharply lower valuation.

The June 8 report was prepared by FMS research head Mark Angeles and research analyst Shane Tan.

Long considered a bellwether for the property sector and a stock that commanded a premium valuation, Ayala Land has lost more than 40 percent of its market value since the start of 2026, making it the industry’s worst performer.

The stock is now trading at P13.40 each, its lowest level in about 15 years.

Housing slowdown

According to FMS, the company’s residential segment, which accounts for about 60 percent of operating earnings, remains under pressure as elevated interest rates continue to dampen housing demand.

The property sector has endured a string of setbacks in recent years from the POGO exit and a growing condominium oversupply to the flood control controversy. It now faces the prospect of higher borrowing costs as the central bank signaled further rate hikes to tamp down inflation pressures linked to the US-Iran conflict.

The warning signs became more evident in the first quarter, when Ayala Land reported a 23 percent drop in net income to P5.4 billion alongside a 14 percent decline in revenues.

Ayala Land’s debt wall

The brokerage also cited concerns over debts maturing this year, a burden that has prompted management to scale back capital spending plans to P50 billion from P93 billion previously.

(FMS later clarified that P25 billion of the debt classified as current had already been refinanced as of May, while the remaining P55.6 billion consists of revolving credit facilities that are routinely renewed. Still, FMS cautioned that Ayala Land's debts remain elevated relative to its real estate peers.)

While its balance sheet remains sound, FMS said the risk of slower earnings growth and heavy debts limits Ayala Land's ability to fund expansion and unlock value from its vast land bank.

Ayala Land has also turned to malls, offices and hotels to generate recurring income, but FMS said those businesses are unlikely to fully offset weakness in residential sales anytime soon.

Lost premium

FMS estimated Ayala Land’s assets are worth about P32.2 per share, but applied a steep 50 percent discount, arguing that investors may have to wait much longer for those assets to translate into profits and cash returns.

The brokerage arrived at its P15.5 target price by assessing the earnings potential and underlying value of Ayala Land’s various businesses while adopting a more cautious outlook to reflect slower growth, rising risks and a tougher operating environment.

MSCI risk adds to pressure

Those assumptions led FMS to conclude that investors should value Ayala Land at only about 60 centavos for every peso of net assets on its balance sheet, a rare stance for one of the market’s traditional blue-chip growth stocks.

Adding to the risks, Ayala Land faces a high probability of being removed from the MSCI Philippines Standard Index by August, according to FMS, potentially triggering selling by foreign funds that track the benchmark.

Editor’s note: This article has been updated to reflect the clarification that debt maturities in Ayala Land's financial records had been refinanced as of May 2026.

Miguel R. Camus has been a reporter covering various domestic business topics since 2009.