That initial public offering (IPO) raised nearly P5 billion, drawing a wide range of investors, including Philippine state pension funds seeking stable but growing dividend-paying stocks.

But years later, the Vista Land & Lifescapes Inc. subsidiary continues to lag behind and its share price has lost 21 percent this year.

This would typically lure dividend yield hunters, but Abacus Securities’ research head Nicky Franco said investors should think twice.

Instead, he raised red flags over VREIT’s ballooning multibillion-peso uncollected rents, warning that these could eventually undermine the firm’s ability to sustain dividends to stockholders.

27 months of unpaid rent

In a note to investors last Oct. 2, Franco zeroed in on the firm’s accounts receivables—amounts billed but not yet collected—totaling almost P5.4 billion as of June this year. This is 16.4 percent higher than the end of 2024.

He noted these already amounted to 27 months of rent revenue.

The uncollected earnings are about 350 percent larger than VREIT’s revenues of P1.2 billion in the first half of 2025 and more than double the rentals earned in 2024.

Huge gap between rentals booked and actual collections

The situation raises bigger questions about the business operations of Villar’s real estate empire.

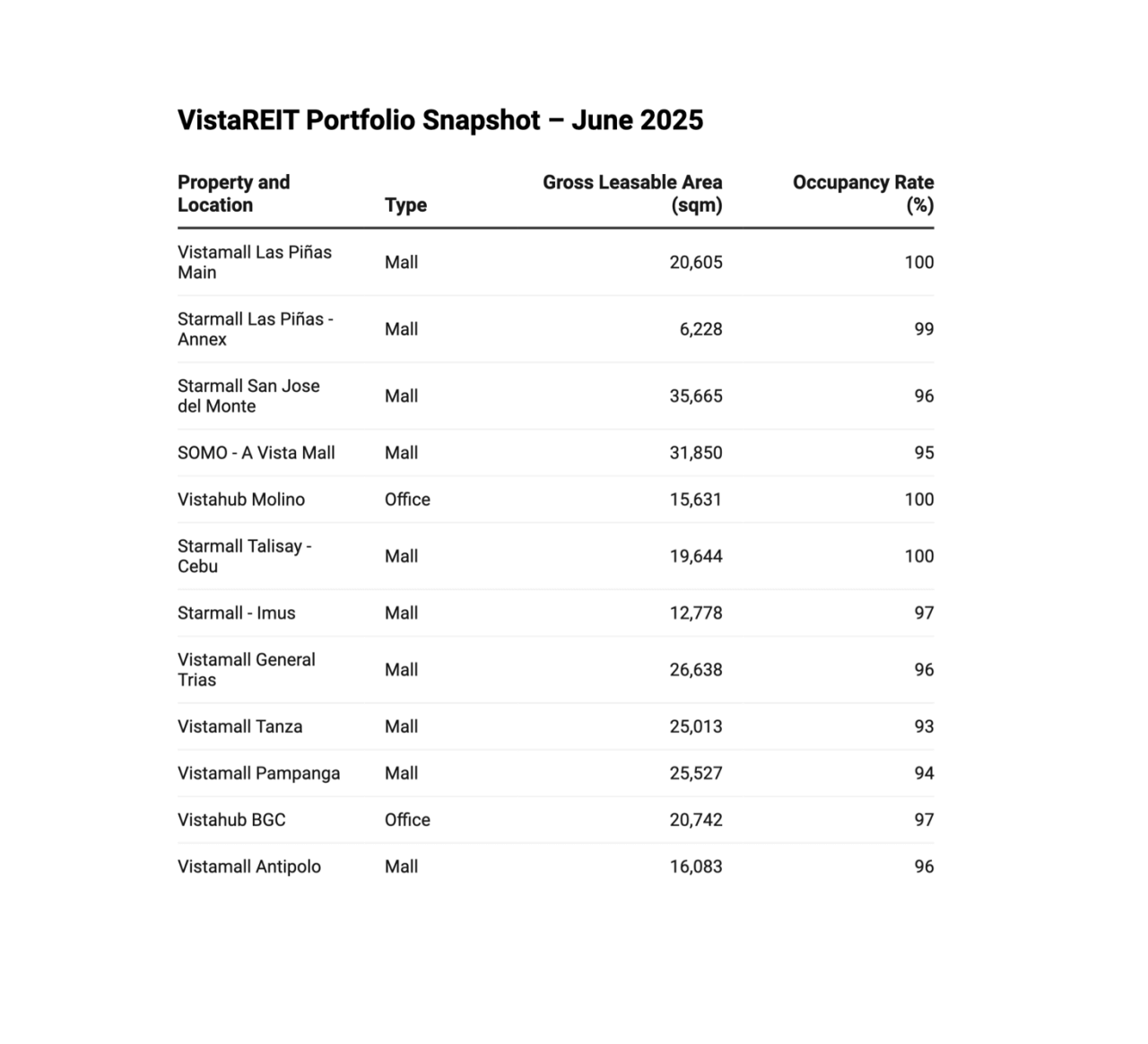

Why are debts from tenants soaring when its malls and offices boast occupancy rates of 93–100 percent as of end-June 2025?

“On our calculations, the firm has collected only about 30 percent of rents in 2023, 2024, and [the first half of 2025],” Franco explained.

Villar firms owe billions to VREIT

Step into any VREIT establishment and it’s clear there are strong synergies with other parts of the tycoon’s businesses—from AllDay Supermarkets and AllHome DIY stores to AllBank, Coffee Project cafés, and convenience stores.

The problem is, many Villar-linked affiliates are way behind on rent payments.

In a section of VREIT’s 2024 report down receivables, it showed that P3.7 billion came from related parties, meaning Villar Group affiliates.

This was the bulk of receivables at the time and this trend likely continued in the first semester of 2025.

VREIT said the obligations are guaranteed by unlisted parent firm Fine Properties Inc.

This could help explain why neither management nor its external auditor, SGV & Co., has recognized significant impairment losses for these unpaid rents.

What’s going on with VREIT’s earnings?

When a landlord fails to collect rent, this should hurt profits, right?

Not necessarily. VREIT uses straight-line accounting for rental income, meaning expected rents are spread evenly over the entire lease term—even if tenants don’t pay on time.

This approach is allowed under accounting rules, but the problem is the ballooning receivables now running into the billions, which is why it was flagged by Abacus’ Franco.

Fair value gains lift profits

Instead of posting lower earnings, VREIT reported a 6.7 percent increase in net income to P733.1 million during the first semester, despite the decline in revenues.

VREIT attributed the gain to what it described as a “normalized recognition” of rental income.

This accounting adjustment on fair value changes to its properties effectively turned last year’s P230.4-million loss into a smaller P148.3-million loss for this period.

Profits are crucial for REIT investors since these firms are required to distribute at least 90 percent of their income as dividends.

It’s not the first time a Villar company has leaned on asset revaluations in its business. Last March, Villar Land announced record 2024 profits from a more than P1-trillion land revaluation, but this was later rejected by its external auditor.

Stock price decline

VREIT’s share price drop has raised its implied dividend yield to about 13 percent, according to the Merkado Barkada REIT index.

The only other REIT with a similar yield is Villar-backed Premiere Island Power REIT Corp., whose share price had plunged over 53 percent this year after the government canceled the operating permit of one of its affiliates in Siquijor.

Other REIT firms have seen gains this year led by Ayala Land’s AREIT (+11.8 percent), DDMP REIT (+1.9 percent), Filinvest REIT (+11.9 percent), RL Commercial REIT (+28.5 percent), MREIT (+3.3 percent), and Citicore Energy REIT (+20.7 percent).

The bottom line

The question for VREIT is how long it can sustain growth and profitability before changing course and collecting the mounting rents that remain unpaid.

“It is remarkable, in our view, that management has not recognized significant provisions on such a large receivables balance, and this may eventually catch the attention of regulators,” Franco said.

“And unless rectified soon, there is likely to be pressure on VREIT’s ability to pay dividends. We now believe, therefore, that its 13 percent yield is not sufficient to compensate for the stock’s inherent risks,” he said.

“Avoid VREIT until the receivables picture improves significantly,” he concluded.

Miguel R. Camus has been a reporter covering various domestic business topics since 2009.