• Net income up 19.1 percent to P15.2 billion

• Revenues climb 9.4 percent to P36.6 billion

• Earnings before interest, taxes, depreciation and amortization at P25.3 billion with 69.0% margin

• Record capital spending of P26.9 billion

• Cash dividends declared at P8.44 billion or P1.14 per share

Maynilad Water Services Inc. delivered double-digit profit growth in 2025, pairing stronger margins with record investments and a dividend that beat its own minimum target.

The west zone concessionaire of Metro Manila Net said net income last year climbed 19.1 percent to P15.2 billion from P12.8 billion in 2024.

Revenues rose 9.4 percent to P36.6 billion from P33.5 billion, driven mainly by approved tariff adjustments and steady billed connections.

Cash operating expenses increased just 1.5 percent, widening the gap between income and costs. Earnings before interest, taxes, depreciation and amortization jumped 14.9 percent to P25.3 billion, with margin expanding to 69 percent.

Dividend sends a message

The board approved a cash dividend of P1.14 per share, totaling about P8.44 billion, payable in March.

The payout exceeds the minimum under its amended policy, reinforcing management’s confidence in cash flow and its long-term capital program.

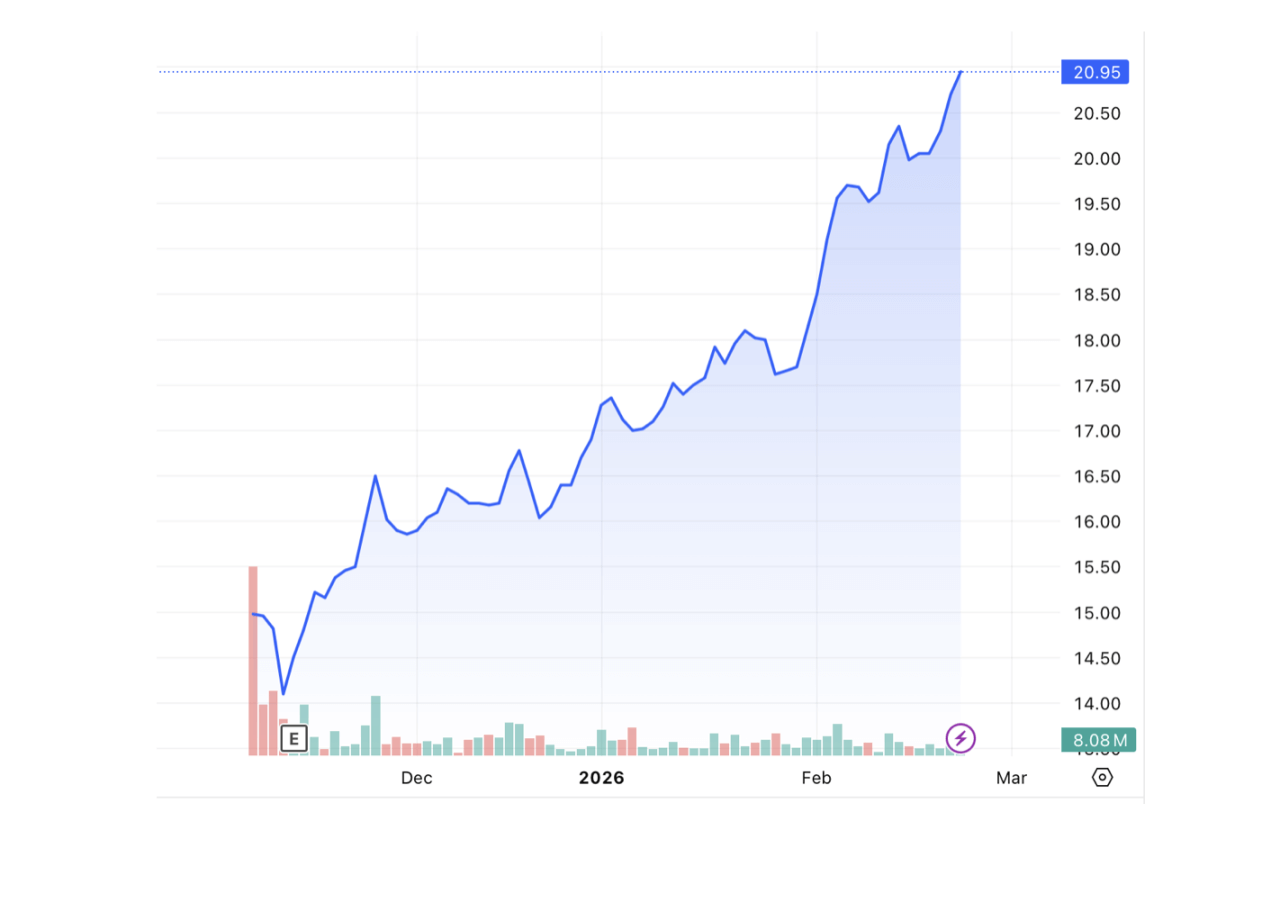

Maynilad, which went public in November last year, has gained nearly 40 percent since listing with its last closing price of P20.95 per share.

Management’s view

“We delivered double-digit growth in net income and EBITDA, sustained margin improvement, and achieved our highest capital disbursement to date. At the same time, we continued to reduce non-revenue water and expand wastewater coverage,” said Ramoncito S. Fernandez, president and CEO.

“The board’s dividend declaration, which exceeds our minimum policy commitment, underscores the strength of our cash generation and confidence in our long-term capital program,” he added.

Big spending, bigger asset base

Capital expenditures surged to P26.9 billion, the highest in the company’s history, funding water supply upgrades, pipe replacements, and sewer expansion.

These investments lifted the interim cash position to P163.9 billion at the start of 2026, up 63 percent from the opening cash position of P100.4 billion at the beginning of the current rate rebasing period. T

he regulated asset base supports a 12 percent pre-tax nominal return under the revised concession agreement, tying future earnings to continued capital deployment.

Service gains show up

Operational indicators improved alongside financial results. Average non-revenue water dropped to 34.9 percent from 39.9 percent, with year-end levels down to 30.7 percent.

Sewer coverage expanded to 26.5 percent, while 24 seven water service reached 91.9 percent, signaling broader and more reliable service delivery.

—Edited by Miguel R. Camus